Bringing Private Health Insurance Into the 21st Century

A plan for blending the best aspects of American health care with market-based models abroad.

Executive Summary

The U.S. does not have a “free market” health care system. 90 percent of Americans have health insurance, nearly all of whom have their coverage heavily subsidized by the government. Indeed, on a per-capita basis, the U.S. spends more than nearly every other country in the world on health care subsidies.

Private coverage is not the same thing as market-based coverage…There cannot be markets where choices are absent and prices opaque.

Part of the misconception stems from the fact that 159 million Americans receive health insurance through their employers. Private coverage is not the same thing as market-based coverage. Thanks to long-standing distortions in the tax code, few workers have the opportunity to choose their own coverage, in a transparent market where prices and benefits are easy to understand. There cannot be markets where choices are absent and prices opaque.

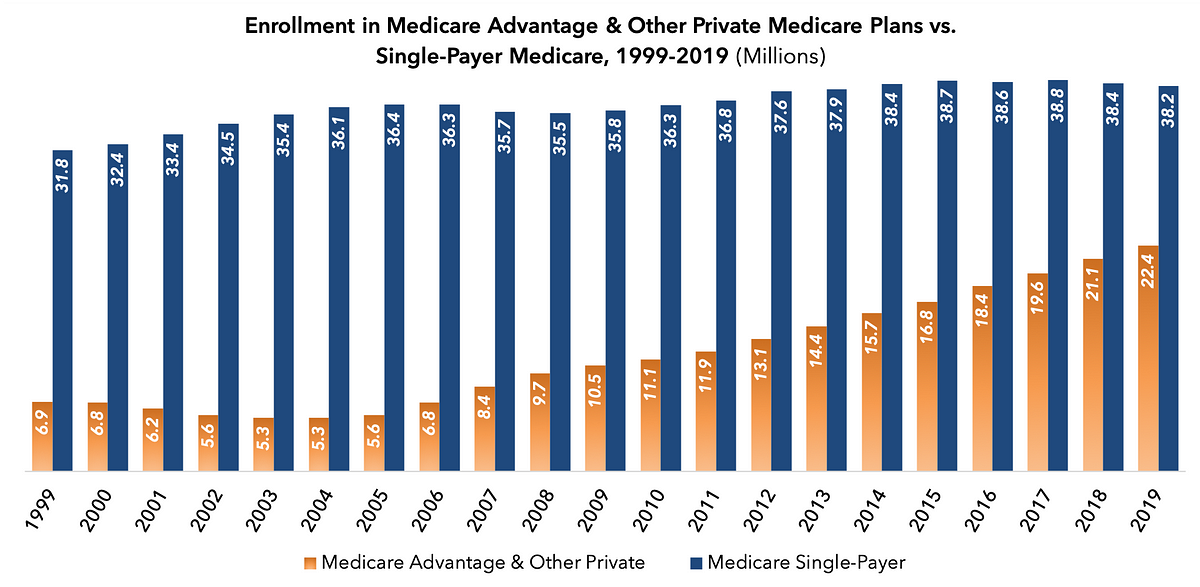

Similarly, those on the left supporting “Medicare for all” falsely equate Medicare with single-payer health care. While it is true that the traditional 1965-vintage version of Medicare is a government-run, single-payer program, Medicare Advantage is, in many ways, the opposite: a market-based system with robust choice and meaningful price signals. Medicare Advantage, in these ways, is significantly more market-oriented than the employer-based system. Medicare Advantage’s popularity has soared, while enrollment in single-payer Medicare is actually declining.

The Affordable Care Act’s changes to the individual market have made it more attractive to uninsured individuals with pre-existing conditions, but they have also made it far less attractive to uninsured individuals who are relatively healthy, with skyrocketing premiums and limited choice. Contrary to conventional wisdom on both the left and the right, solving the latter problem does not require unsolving the former one.

In this paper, we explore these and many other misperceptions of market-based health insurance in America. We identify several key factors that characterize the most successful health insurance markets in America and abroad:

- Freedom of choice among a broad range of insurance plans;

- Consumer-driven incentives for insurers to offer lower prices, higher quality, and better value;

- Access to innovation in terms of new medical technologies and new models of care management and delivery;

- Access to doctors with minimal delays or waiting lists;

- Underlying costs that are affordable for unsubsidized enrollees; and

- Fiscal sustainability of subsidized programs, in terms the scale of subsidies, their growth rate, and their demographic balance.

Truly market-based health insurance would cost much less, be more fiscally sustainable, and provide far greater choice and consumer satisfaction than the system we have in America.

Indeed, it is essential that policymakers not be complacent about the status quo, and recognize that Americans have good reason to be deeply dissatisfied with the high cost and low choice of today’s employer-based system. In a survey of 62,000 respondents ranking 188 brands in 23 industries using the Net Promoter Score—a widely used measure of consumer loyalty—the health insurance industry ranked third-to-last, only ahead of cable and satellite TV providers and internet service providers.

The good news is that there are ways to meaningfully improve private health insurance in the United States, by adapting best market practices throughout America’s private health insurance programs. Our recommendations include:

- Transition to a system in which employers fund Health Reimbursement Accounts that workers can use to buy health insurance on the individual market;

- Lower premiums in the individual market by deploying integrated high risk pools through reinsurance, and other reforms;

- Expand affordable choices in the individual market through broader offerings, state flexibility, and reform of the Affordable Care Act’s subsidy structure;

- Expand the ability of enrollees in public programs, like Medicare and Medicaid, to choose private coverage; and

- Increase insurer competition by requiring transparency into anticompetitive payer-provider contracts.

We believe that these reforms, combined with others described in our broad reform plan, Medicare Advantage for All, can make health insurance affordable for every American living today, while also enabling our health care system to be fiscally sustainable for the generations to come.

Introduction

The partisan debate about health reform in America is built upon a fundamental misperception: that the U.S. health care system represents a “free market.”

Both the Left and the Right commonly describe America’s health care system as “free market,” in contrast to those of the social democracies of western Europe. For the Left, this is seen as a flaw to be corrected; for the Right, it is a virtue to be preserved. For better or worse, however, the United States has not had a free-market health care system for generations.

For example, in 2013, according to the Organization for Economic Co-operation and Development (OECD), U.S. government entities collectively spent $4,160 per capita on health care, the third-highest such total in the world.

Notably, these figures represent America’s standing prior to the implementation of the ACA’s spending provisions in 2014. On a per-capita basis, the vast majority of universal health care systems in the industrialized world spend less taxpayer money than does that of the U.S. It is a testament to how profoundly costly American health care is, that tens of millions remain uninsured despite this extraordinary level of public spending.

On the Left, these data are used to argue that market-based health care cannot keep health care costs in check. But that is not the case. As the table above shows, Switzerland—a country with a universal system of private health insurance and no “public options”—has one of the most fiscally sustainable health care systems in the world.

Indeed, Switzerland has achieved universal coverage with 45 percent less public spending than the United States. Put another way: if America had Switzerland’s health care system, the U.S. would not have a debt and deficit crisis. How did Switzerland do it?

What a market-based health care system looks like

Before considering the Swiss model in more detail, it is important to contemplate what a market-based health care system looks like.

No industrialized nation has a libertarian health care system in which the government plays no role in subsidizing or regulating health insurance. However, there are a number of market-based models in which private insurance plays a primary if not exclusive role, and where consumers have a meaningful amount of choice in the cost and design of the coverage they buy. The characteristics of a market-based health care system include:

- Freedom of choice. Unlike in a single-payer system, in which the only available insurer is a government agency, market-based systems give consumers the ability to choose among a broad range of private health insurance options, so that they can find one that best suits their needs. Choice also creates the opportunity for new models of insurance to evolve, with additional benefits or features that would not have been feasible or desirable in past decades.

- Consumer-driven incentives. In a market-based system, consumers are price-sensitive: that is to say, if they consumer costlier services or coverage, they will have to cover a meaningful amount of the cost. Price sensitivity is critical, as it incentivizes insurers to deliver coverage at the lowest possible price, through innovations in care management and through efficient price negotiations with hospitals, doctors, and drug companies. While many market advocates talk about “price transparency,” they often focus on the small minority of health care services paid for out-of-pocket. Three-fourths of American health care is paid through insurance; price transparency around insurance premiums is critical.

- Access to innovation. Because single-payer systems are frequently “free” at the point of care, governments deploying such systems ration access to new technologies. Government systems also lack the flexibility to incorporate new ideas in health care delivery. Market-based systems are more open to medical innovations that improve health, extend lives, and lower costs.

- Access to doctors. Single-payer systems often suffer from a low supply of participating physicians, leading to long wait times for care. In market-based systems, patients have broad, though not necessarily unlimited, access to medical care, with low wait times and strong customer service.

- Underlying cost. If market-based systems are working well, and insurers are competing for individuals’ enrollment on the basis of price and quality, the underlying cost of insurance should be affordable for the average individual before subsidies are taken into account.

- Fiscal sustainability. Health care spending throughout the industrialized world often grows at a pace that exceeds economic growth. This is particularly dangerous for heavily subsidized systems, because the growth in subsidies can exceed the ability of taxpayers to fund them.

So: how many Americans participate in something that can be fairly called market-based health insurance? The United States has a highly fragmented health care system. Roughly 90 percent of legal U.S. residents have health insurance, but the way in which Americans obtain coverage varies widely.

Over 100 million Americans are on single-payer, government-run health insurance, provided by the traditional Medicare program, Medicaid, the Children’s Health Insurance Program, or the Veterans Health Administration. Over 50 million receive coverage from market-based programs with a range of private insurance choices: Medicare Advantage, the Federal Employees Health Benefits Program (FEHBP), and the individual health insurance market. Another 151 million non-federal employees receive private coverage from their employers.

It is worth reviewing these systems against the standard of market-based health insurance that we defined above.

Employer-sponsored insurance

Overall grade: C-minus

2019 enrollment: 151 million (excluding members of the Federal Employees Health Benefits Program)

While employer-based health insurance coverage is commonly thought of as America’s “market based” health insurance system, it departs considerably from market principles. Employers rely on the largest and fastest-growing subsidy in the tax code—the exclusion from taxation of the value of employer-sponsored insurance (ESI)—to offer coverage to half of all Americans. The Joint Committee on Taxation estimates that fiscal value of this tax break in 2019—in terms of lost revenue to the federal government, and/or lower taxes elsewhere—is 1.4 percent of GDP, or roughly $300 billion. The value of the exclusion from state and local taxation represents an additional $38 billion, for a total of $338 billion. (Fiscal sustainability: C).

Because ESI premiums are taken out of a worker’s paycheck before he receives it, employees rarely understand how much of their compensation is taken up by the cost of health care. They demand access to costly services because they lack the tools to understand how costly services affect their health insurance premiums. (Consumer-driven incentives: D)

This lack of price sensitivity, in turn, has led the cost of employer-based coverage to explode. Indeed, American ESI is the costliest form of health insurance in the world. (Underlying cost: F)

Furthermore, workers in the ESI system rarely get to choose their health insurer; instead, that insurer is chosen on their behalf by a human resources executive at their employer. However, an increasing number of employers are deploying high deductibles and other cost-sharing tools to keep costs down; average deductibles have tripled in the last decade. As a result, more workers are gaining access to tax-advantaged Health Savings Accounts and Health Reimbursement Accounts, which provide improved choice for routine health care expenses. (Freedom of choice: D)

In general, however, employers know that their employees are not price sensitive, and see generous health benefits as a retention tool. As a result, they have been reluctant to limit access to costly providers or health care services, out of fear that workers will rebel and decamp to a rival employer. (Access to doctors: A; Access to innovation: A)

For all these reasons, economists have long sought to curtail the ESI tax exclusion. They have had limited success.

In 2008, Republican presidential nominee John McCain campaigned on replacing the employer tax exclusion with a universal tax credit of $2,500 per individual or $5,000 per family. Despite the fact that the $2,500 individual tax credit is slightly more generous than the existing value of the tax break for employer-sponsored insurance, and would apply to all Americans, including the uninsured, then-Sen. Barack Obama spent over $100 million on a campaign ad that attacked the plan because it would “tax health benefits for the first time ever, meaning higher income taxes for millions.”

After Obama became President, however, his signature health reform—the Affordable Care Act—did something quite similar to McCain’s proposal, applying a “Cadillac tax”—a 40 percent excise tax—to expensive employer-based plans, and using the funds to pay for tax credits for the uninsured. Indeed, the Affordable Care Act is the law that “taxed health benefits for the first time ever.”

Congress has repeatedly put off the start date for the imposition of the Cadillac tax; when the ACA was passed, it was supposed to go into effect in 2018. After several amendments by Congress, the Cadillac tax is now scheduled to take effect in 2022, and applies the 40 percent tax to the value of health benefits exceeding $11,200 for individuals and $30,150 for family coverage.

Federal Employees Health Benefits Program

Overall grade: B-minus

2019 enrollment: 8 million

The Federal Employees Health Benefits Program, or FEHBP, is a form of employer-sponsored health insurance. But it deserves separate treatment from traditional ESI, because it contains some market-based features that conventional employer-based insurance lacks.

8 million federal employees participate in FEHBP, which gives workers an average of 24 health insurance offerings (Freedom of choice: A-plus), compared with just one or two in conventional ESI. Taxpayers fund 72 percent of the weighted average premium of all plans, not to exceed 75 percent of the premium for any given plan; this amounts to nearly a $7,000 per year subsidy from taxpayers (Fiscal sustainability: C).

Since federal employees do save some money if they choose a less-expensive plan, there is an element of price sensitivity to the FEHBP (Consumer-driven incentives: B), but the very generous subsidy incentivizes federal workers to choose costly plans with low deductibles and high premiums (Underlying cost: F). The generosity of these plans, and their high cost, means that federal employees have very broad access to hospitals and doctors, including high-cost providers (Access to doctors: A-plus; Access to innovation: A).

Medicare Advantage

Overall grade: B-plus

2019 enrollment: 22 million

Medicare Advantage, alternatively known as Medicare Part C, is the program that administers the Medicare benefit package—hospital care and outpatient physician care—through private insurers. Medicare Advantage plans commonly cover additional services, such as vision, dental, and prescription drugs. Enrollment in MA is growing at a rapid pace, because private insurers are delivering the basic Medicare benefit at a lower cost than traditional Medicare, with better health outcomes.

Seniors in MA can select from 21 different plans, on average, and are expected to pay the difference if plans exceed the cost of Medicare’s premium benchmark (Consumer-driven incentives: B). That provides a meaningful incentive for insurers to compete on price, though the structure of Part C limits the utility of price competition. (For a thorough discussion of this issue, please see Medicare Advantage: A Platform for Affordable Health Reform.)

But despite those limitations, the intense competition among Medicare Advantage plans for market share is leading to a golden age of managed care innovation, deploying 21st-century data science, machine learning, artificial intelligence, wearable technologies, and novel delivery models (Access to innovation: A-plus).

To take one example, in January 2019, CNBC reported that Apple was in talks with “at least three private Medicare plans about subsidizing the Apple Watch for people over 65 to use as a health tracker.” Some of these insurers are established players, according to the report, whereas others are venture-backed startups. “Avoiding one emergency room visit would more than pay for the advice,” observed Bob Sheehy, CEO of insurance startup Bright Health.

Medicare Advantage plans are highly affordable for seniors, primarily because they are extremely heavily subsidized by younger taxpayers, as all Medicare plans are (Fiscal sustainability: D).

But Medicare Advantage plans also do a far better job than other plans at negotiating payment rates with hospitals and doctors, because providers outside of MA networks are generally required to accept traditional Medicare’s reimbursement rates (Underlying cost: C-plus; Access to doctors: A). By contrast, the average employer-based plan pays more than double what Medicare pays for hospital care. And unlike traditional, single-payer Medicare plans, Medicare Advantage plans are required to offer seniors an out-of-pocket cap, offering catastrophic coverage where traditional Medicare does not.

Individually-purchased health insurance

Overall grade: B

2019 enrollment: 13 million

The market for Americans who buy health insurance on their own—as opposed to through the government or their employer—was transformed by the Affordable Care Act, starting in 2014 when the ACA’s novel layer of federal regulations went into effect. The best-known of those regulations requires insurers to offer coverage to those with pre-existing conditions, also known as guaranteed issue.

But the law contains a blizzard of other, less-well-known regulations, the result of which has been an explosion in the cost of individually-purchased health insurance, especially for uninsured Americans below the age of 45, those in average health or better, and those with incomes above $30,350 for childless adults and $62,750 for families of four (i.e., above 250 percent of the Federal Poverty Level). In effect, the ACA subsidizes coverage for uninsured Americans who are sick by overcharging uninsured Americans who are healthy (Underlying cost: D). These high premiums are not accompanied by low deductibles; indeed, the median deductible for a benchmark Silver plan in 2019 was $4,375.

The regulatory intrusion represented by the ACA, combined with chaotic enforcement by the Obama administration, has kept many insurers out of the ACA’s health insurance exchanges. In 2019, the average individual market enrollee could choose from among four insurers, and those plans had little room for variation from each other, outside of provider network design (Freedom of choice: C).

Remarkably, the number of people enrolled in the individual market is roughly unchanged from prior to the ACA; in 2013, prior to the ACA taking effect, approximately 13 million people purchased coverage in the individual market. Today, 13 million people are in the individual market: 9 million on the ACA exchanges (7 million with premium subsidies); 4 million outside the exchanges; and 1 million through the Basic Health Program, a version of the ACA exchanges organized at the state level.

As the chart above illustrates, in 2010, the Congressional Budget Office projected that 24 million Americans would enroll in the exchanges in 2019; the actual figure was closer to 9 million.

The news is not all bad, however. The ACA’s sliding scale of subsidies, modeled after Switzerland’s, allows for financial assistance for sick and low-income enrollees, while gradually phasing out up the income scale so as to mitigate the problem of “subsidy cliffs” which disincentivize low-earners from raising their income by, for example, working longer hours.

The ACA’s insurance exchanges deploy the best pricing signal of any system in America: competitive bidding based on the second-least-costly Silver plan (i.e., a plan with an actuarial value of 70 percent) in a given geographic area. In 2019, for example, the average premium for the second-least-costly Silver plan was $477 per month. Enrollees who choose a different plan, costing $500 per month, would be responsible for the extra $23. Unfortunately, those who choose a plan less costly than the benchmark $477 per month do not capture the savings; however, the competitive bidding process gives insurers an incentive to propose the lowest possible price (Consumer-driven incentives: B+). This stands in contrast to Medicare Advantage, where the federal government sets the rate at which plans are paid, by relating it to what single-payer Medicare costs to cover the same patient.

Importantly, Section 1401(b)(3)(ii) of the ACA contains a fiscal “failsafe” that specifies that once ACA premium and cost-sharing subsidies exceed 0.504 percent of gross domestic product—approximately $108 billion in 2019 GDP terms—the aggregate amount of those subsidies can only grow at the same rate as the overall consumer price index. While the 0.504 percent threshold will not be breached in the near term—the Congressional Budget office projects that aggregate subsidies will remain below $100 billion through 2029—the failsafe aligns subsidy growth with consumer inflation, rather than U.S. health care inflation: a key requirement for long-term fiscal sustainability (Fiscal sustainability: A).

Individual market insurers tend to pay providers in a similar fashion to Medicare Advantage and employer-sponsored coverage, leading to reasonably broad access to care and innovative technologies (Access to doctors: A-minus; Access to innovation: A).

The Swiss health care system

Overall grade: A

2019 enrollment: 9 million

It is worthwhile to compare each of the American models of private health insurance to the world’s gold standard in market-based health insurance: Switzerland. While the Swiss system is not perfect, and would benefit from targeted reforms, overall it represents the best real-world model of how competitive markets can deliver universal coverage through private insurance.

The modern Swiss health care system arose from reforms that were enacted in 1996, establishing a universal, market-based health insurance system. In Switzerland, there are no “public option” government-run insurers like Medicare or Medicaid; instead, everyone purchases private insurance on a robust individual market, with 26 regional insurance exchanges.

Consumers have a choice of plans with deductibles of 300, 500, 1,000, 1,500, 2,000, and 2,500 Swiss francs, with an out-of-pocket cap of CHF 700 above the deductible; the Swiss franc is roughly equivalent to the U.S. dollar. Price transparency is straightforward, with all insurer prices easily available online. Insurers are allowed to vary premiums by age, sex, and hospitalizations in the previous year. Like Americans, the Swiss have the option to select managed care plans with narrower networks of providers, in exchange for lower premiums. Indeed, the average Swiss resident has a choice of 59 insurers (Freedom of choice: A-plus).

While health care in Switzerland is slightly costlier than in other European countries, it is far lower than it is in the United States (Underlying cost: B-plus). Switzerland, a wealthy country, spends 12 percent of GDP on health care, compared to 18 percent in the U.S. A key feature of cost control in Switzerland is that the Swiss allow insurers at the cantonal level to jointly negotiate reimbursement rates for hospital services, balancing out the natural monopoly power of providers. Branded drugs are only subsidized by insurance if they are shown to be clinically effective, cost effective, and appropriate for a given disease.

Swiss public spending on health care is roughly half that of the U.S., because only poorer and sicker citizens receive financial assistance (Fiscal sustainability: A-minus). In the U.S., nearly everybody receives a substantial subsidy to buy health insurance, regardless of need. Indeed, in the employer-based system, the highest earners receive the largest tax subsidy, because their income tax rates are the highest, and therefore the exclusion of health insurance from taxable income is of greatest monetary value for them.

Switzerland subsidizes, on a sliding scale, the premiums its citizens pay for private health insurance: a system known in the U.S. as “premium support.” In Switzerland, low-income individuals are fully subsidized; middle-income individuals are modestly subsidized; and upper-income individuals are not subsidized. Individual Swiss cantons, the equivalent of U.S. states, have the flexibility to alter the formula by which subsidies phase out; as the above chart demonstrates, Swiss cantons reflect a wide variety of approaches.

The sliding subsidy scale mitigates one of the key challenges with traditional welfare programs, in which recipients are no longer eligible for a defined benefit once their income exceeds a specified threshold. These “benefit cliffs” discourage welfare recipients from seeking additional work, because by increasing their wage income, they are decreasing their overall income, once the value of the rescinded welfare benefits is taken into account.

Like Americans in the private market, Swiss citizens are fully able to choose their doctor, and enjoy broad access to innovative technologies (Access to doctors: A; Access to innovation: A).

Adapting from the best real-world market-based models

What would an ideal blend of these various private-sector health insurance systems look like?

Learn from Switzerland on reducing the cost of care. By far, the biggest problem with American health care is its cost. Cost is the reason that tens of millions of Americans are uninsured, and why tens of millions more are insured, but struggling to afford their coverage. This problem is especially acute with employer-sponsored insurance.

Swiss health insurance is about half the price of American coverage. Two key features of the Swiss system stand out in this regard:

- Strong consumer-driven incentives for lower cost. Because each Swiss resident buys insurance on his or her own, and are economically rewarded for choosing lower-cost plans, health insurance in Switzerland works much like auto insurance in the U.S., in which coverage is universal, and insurers have an incentive to negotiate effectively on consumers’ behalf. These features are especially absent in the employer-sponsored market, where workers need and deserve more choice. One way to expand choice in the employer market is to allow workers to use employer-funded Health Reimbursement Accounts to purchase individual-market coverage.

- Tools for curtailing monopoly power. In the U.S., regional hospital monopolies and prescription drug monopolies demand high prices from insurers, who lack the negotiating leverage (and, in employer-sponsored coverage, the strong incentive) to fight back. Switzerland addresses this problem in part by allowing insurers in a given canton to jointly negotiate prices with regional hospital monopolies. Medicare Advantage deploys an alternative mechanism: using Medicare’s fee-for-service rates as a way of capping the pricing power of hospital monopolies. Medicare has proven less effective at controlling the cost of physician-administered drugs, though recent initiatives from the Trump administration may lead to progress in this regard.

Strengthen the individual market for health insurance. While market-based features can be added to every patch of the U.S. health care system, the most important—and most sustainable—path to market-based universal coverage is to strengthen the individual market for health insurance.

The individual market increases consumer satisfaction, reduces costs, and expands innovation. In the U.S., the individual market is also the most fiscally sustainable private market, because over the long term, growth in ACA premium and cost-sharing subsidies is tied to consumer inflation. This fiscal failsafe in the ACA, in turn, gives insurers a powerful incentive to hold the line on costs.

Strengthening the individual market requires important reforms—correcting the Affordable Care Act’s key design flaws—so that individual-market premiums are actually affordable for more people.

It also involves enlarging the individual market, so that more insurers have an incentive to participate, creating a virtuous cycle of competition, innovation, and cost reduction.

The remainder of this paper focuses on reforms that could achieve these objectives.

Drawbacks of the ACA exchanges

Apart from the basic aim of expanding health coverage, the authors of the ACA exchanges sought to achieve several objectives by heavily regulating the individual insurance market.

Their first goal was consumer protection. They required that all participating insurers offer plans to anyone who sought one (guaranteed issue). They also required that plans compete on the basis of standardized financial benefits (actuarial value), so that consumers would not have to worry that a plan’s fine print would leave them with unanticipated medical expenses.

Their second goal was redistribution. They forbade plans from charging lower premiums to healthier individuals, and constricted the ability of plans to charge lower premiums to younger enrollees (“community rating”).

They required insurers to charge the same rates to men and women: in effect, a redistribution from men to women, because women, on average, consume more health care services. They required all plans to cover services (“essential health benefits”), such as drug addiction therapy, that few people might need: in effect, requiring all insured individuals to subsidize those services on behalf of the minority who use them.

Their third goal was utility conversion. They sought to convert the existing private insurers into regulated utilities, whose rates and operating margins (“medical loss ratios”) would be prescribed and regulated by the federal government. The ACA authors believed that there is a fundamental conflict between the economic interests of insurers and those of patients.

Unfortunately, this approach has significant drawbacks. Most importantly, the ACA significantly drives up the cost of individually purchased health insurance in most of the country. On average, premiums in the individual market have doubled since the ACA went into effect. The ACA imposes these cost increases principally on healthier and younger individuals, and on men more than on women.

A key development took place in December 2017, when President Trump signed into law the Tax Cuts and Jobs Act (TCJA). That law eliminated the penalty connected to the Affordable Care Act’s individual mandate, as of January 1, 2019, effectively repealing it. The individual mandate was one of the key flaws of the ACA—and, incidentally, the biggest flaw of the Swiss health care system. The ACA’s mandate was doing little to encourage individuals to sign up for health insurance, due to its plethora of exemptions and weak enforcement by both the Obama and Trump administrations.

The reason this change is significant is because it fundamentally changes the way the individual market works. Now, insurers and policymakers must work to make health insurance attractive to skeptical consumers, instead of irresponsibly driving up its cost and forcing consumers to buy it anyway.

Proposed changes to the individual health insurance market

- Preserve consumer protections. There are a number of features that the Affordable Care Act standardized in the individual market that will and ought to be preserved. These include the consumer-friendly system of metal tiers — Bronze, Silver, Gold, and Platinum — that allow individuals to easily compare the financial value of competing health plans. They include the “guaranteed issue” requirement that all insurers offer coverage to anyone willing to pay the necessary premium, and the “community rating” requirement that all insurers charge the same premium to individuals of the same age, regardless of health status or gender. Congress should preserve the ACA’s caps on lifetime and out-of-pocket limits for Bronze plans and above so as to ensure that every American has access to the benefits of true insurance: protection from catastrophic financial loss due to illness or injury.

- Integrate high risk pools through reinsurance. A number of states, including Alaska and Maine, have sought waivers from the ACA, under Section 1332 of the law, to implement reinsurance programs for the individual market. Reinsurance programs work by directly funding the cost of care for the costliest insurance market enrollees, relieving other policyholders from the burden of paying for those costs through higher premiums. Actuarial studies estimate that a federally funded reinsurance program of $20 billion per year could reduce premiums by 20 percent, reducing spending on ACA premium subsidies by as much as $15–16 billion. These funds could be administered either through a federal reinsurance program, block grants to states, or a combination of both, under which states could have the option to take the funds in a block grant form, or leave the reinsurance program to the federal government. Reinsurance should explicitly include coverage for maternity care; in this way, individual-market plans can fully fund maternity care while reducing its effect on adverse selection (because young men of the same age face higher premiums under the ACA’s 1:1 gender rating). Outlays for reinsurance funds, net of savings from premium subsidies, should be offset by reduced spending elsewhere.

- Reduce premiums for young people. In dollar terms, 64-year-olds consume about six times as much health care as 19-year-olds. But the ACA forces insurers to charge their youngest enrollees no less than one-third what they charge their oldest enrollees, effectively doubling premiums for younger adults. As those younger adults drop out of the market, premiums for older adults rise, because premiums are determined by the average health care utilization by an enrollee in the plan: a concept known as adverse selection. Restoring 6:1 or 5:1 “age bands,” from the ACA’s 3:1 ratio, can do a lot to bring young people back into the market, reducing premiums for everyone. In addition, Congress should age-adjust the tax credits, along the lines of Section 202 of the American Health Care Act or Section 131 of the Fair Care Act. Because the ACA’s subsidy system caps the percentage of income that any subsidy-eligible enrollee will spend on premiums, older, sicker, and poorer individuals remain protected against unaffordable premiums under this system. In addition, by encouraging healthier and younger individuals to purchase insurance, this approach reduces average individual premiums. An transitional measure could be added to such a reform, for individuals with incomes between 400 and 600 percent of FPL, such that these individuals would be eligible for premium assistance for costs above 11.5 percent of their income. The 600 percent FPL threshold would gradually decrease back down to 400 percent in 2030, resulting in an estimated ten-year outlay of $12 billion.

- Consolidate the Federal Employees Health Benefits Program into the individual market. Today, federal employees receive a substantial taxpayer-funded subsidy—nearly $7,000—to purchase health insurance coverage that is far costlier than that available to most private-sector employees. It would be highly beneficial to merge this program with the individual market, by converting the FEHBP subsidy into a 100 percent subsidy for the second-least-costly Bronze-level ACA plan in the employee’s region. This reform would ultimately double the size of the individual market, strengthening its risk pool and increasing insurer participation. It would also strengthen individual market policymaking, as every employee at the Department of Health and Human Services—and every employee in Congress—would be enrolled in the individual market.

- Allow employer-funded HRAs to pay for individual market coverage. In June 2019, the Trump administration finalized a new rule that would allow employer-funded Health Reimbursement Accounts to be used to purchase individual health insurance coverage. This could transform the individual market, by allowing employer to gain fiscal certainty around their annual health care spend, similar to the way defined contribution pension plans have replaced defined benefit pension plans. It would empower workers, who would have more choices in health coverage than they do with their employers. Congress should strengthen the reform by requiring that all newly incorporated businesses deploy the HRA-based approach in order to deduct the cost of health insurance from their corporate incomes. In addition, as discussed below, Congress should repeal the ACA’s employer mandate, which will free up more people to enroll in individual market coverage.

- Replace the ACA’s “catastrophic” option with Copper plans. The ACA makes available so-called “catastrophic plans” that, in theory, should serve as low-cost, high deductible insurance options. In reality, these plans are are no more affordable than conventional Bronze or Silver plans, and rarely used, because they are not eligible for the ACA’s premium subsidies. Congress should replace the ACA’s catastrophic option with true catastrophic coverage, in the form of a Copper plan with an actuarial value of 50 percent. Copper plans should be exempt from the ACA’s annual out-of-pocket caps, so as to maximize consumer choice. The ACA’s premium subsidies should be usable to purchase Copper plans, allowing more people to find plans with a low or zero premium net of subsidies.

- Repeal ACA taxes that increase premiums. The ACA contains several counterproductive tax increases whose net effect is to increase exchange premiums, and thereby, federal exchange subsidies. These include: the tax on health insurance premiums; the tax on medical devices; the tax on pharmaceutical products; the tax on flexible spending accounts; the tax on medical expenses exceeding 7.5 percent of adjusted gross income; the tax on over-the-counter medicines; and the tax on early HSA withdrawals. All of these taxes should be repealed.

- Increase state flexibility. As noted above, Section 1332 of the ACA gives states a modest amount of flexibility in managing their individual health insurance markets. In 2017, Sen. Patty Murray (D., Wash.) and Sen. Lamar Alexander (R., Tenn.) proposed a bipartisan package of reforms that would fund cost-sharing reduction subsidies, establish Copper plans, and give states more flexibility to pursue Swiss-style variations to the way premium subsidies are distributed. Congress could build on this deal to ensure that states have the flexibility they need to pursue reforms that would allow for more innovation in insurance plan design and reduce regulatory burdens.

- Reward consumers for purchasing less costly plans. Consumer-driven health plans are centered around the principle that patients should be in as much control of their health spending as possible, while still providing an insurance product that protects individuals from catastrophic financial loss. However, under the ACA, if a subsidy-eligible individual wants to buy a plan that is less expensive than his subsidy, the extra money goes to waste. Consumers should be able to have those savings deposited in a Health Savings Account (HSA) that can pay for out-of-pocket expenses. Rewarding consumers for choosing less costly plans gives insurers a powerful incentive to reduce the costs of care.

- Convert ACA cost-sharing subsidies into HSA contributions. The Affordable Care Act includes cost-sharing subsidies to defray the costs of deductibles, co-pays, and other cost-sharing features of exchange-based plans, for individuals with incomes below 250 percent of the Federal Poverty Level. Those with incomes between 100 and 150 percent of FPL are subsidized such that the effective actuarial value of their coverage is 94 percent. Those between 150 and 200 percent of FPL are subsidized to an effective actuarial value of 87 percent. Those between 200 and 250 percent of FPL are subsidized to an effective actuarial value of 73 percent. Under Section 1332 of the ACA, Congress should grant states the flexibility to convert these funds—on a deficit-neutral basis—into Health Savings Account subsidies. In this way, low-income families can retain the value of these subsidies if they do not need to deploy them in a given year.

- Auto-enroll eligible individuals. The IRS encourages employers to auto-enroll their workers into individual retirement account programs like 401(k) plans. Auto-enrollment has had a significant impact on the success and scale of enrollment in IRA programs. Similarly, under Section 1332, Congress should allow states to automatically enroll their residents in a state-assigned default plan and default health savings account, so long as auto-enrollees have the ability to opt out of the enrolled plan if they so choose. In October 2020, the Congressional Budget Office stated that it “refers to people who…have automatic coverage through a default plan as having coverage and counts them when assessing the universality of coverage.”

- Reform open enrollment; add late enrollment penalties. An open enrollment period is the period within which individuals can enroll in insurance coverage that benefits from consumer protections such as guaranteed issue. The ACA’s open enrollment period lasts for six weeks every year, going from early November to mid-December. Congress should give states the flexibility, under Section 1332, to conduct open enrollment less frequently, up to once every five years. Under this system, individuals who choose to forego coverage could do so without paying a fine; however, they could not simply enter and exit the system at will and take advantage of consumer protections such as coverage for preexisting conditions, and cross-subsidies such as community rating. In 2009, Paul Starr of Princeton University first advanced this reform as an alternative to the individual mandate. Starr proposed adapting an analogous provision from Germany, where there is no individual mandate, but where the open enrollment period takes place once every five years. “Congress,” he wrote, “could give people a right to opt out of the mandate if they signed a form agreeing that they could not opt in for the following five years. In other words, instead of paying a fine, they would forego a potential benefit.” Open enrollment reform has an additional attraction: it rewards the development of longer-term health insurance contracts. Insurers that know they will be managing an enrollee’s care for a longer period of time have an additional incentive to engage in prevention, knowing that they are more likely to reap its rewards in the form of better long-term health. As a companion policy, Congress could introduce late enrollment penalties, modeled after those used in the Medicare program, in order to incentivize timely enrollment. The combination of less adverse selection, longer insurance contracts, and late enrollment penalties will lead to a much stronger individual insurance market.

Reforming employer-based insurance

More Americans obtain health coverage through their employers than through any other source. According to the Congressional Budget Office, nearly half of all U.S. residents — 159 million — are enrolled in employer-based coverage in 2019.

Americans don’t expect their employers to provide them with auto insurance or life insurance. The reason that they expect health insurance from their jobs has to do with a historical accident: the tax exclusion for employer-sponsored health insurance.

The history of employer-sponsored health coverage

The tax exclusion is the unintended out- growth of World War II economic policy. Prior to the war, health insurance was rare: health technology was in its infancy, and most medical care still took place in patients’ homes.

But in 1929, a group of teachers in Dallas — spurred by their increased need for hospital services — came together and signed an agreement with Baylor University Hospital under which the teachers would pay $6 a year in exchange for 21 days of hospitalization.

The plan grew to cover additional employee groups in Dallas; eventually, the American Hospital Association encouraged other hospitals to adopt similar plans. Hospitals liked the idea because it gave them more predictable income streams and ensured that their bills were paid; beneficiaries, meanwhile, enjoyed the advantages of insurance.

Thus the Blue Cross system was born.

The system offered several advantages to patients as well as providers. The AHA required that Blue Cross–branded plans allow beneficiaries to freely choose their doctors and hospitals. Blue Cross plans charged sick and healthy people similar premiums (i.e., community rating). And because they were organized as nonprofit corporations, insurers enjoyed tax-exempt status and were freed from certain insurance regulations that would have required them to keep assets in reserve against potential claims.

Soon, physicians began establishing similar plans for their own services under the Blue Shield label. Both Blue Cross and Blue Shield plans served a significant number of low-income patients — but the secret of their success was covering large populations of healthy, employed workers.

As a result, the plans were able to build a large pool of clients who did not often require expensive care; the savings from these patients went toward covering the costs of those who did need frequent or expensive care.

For-profit insurers came to notice the success of Blue Cross and Blue Shield, and began to enter the health insurance market. They did not have community-rating rules, and so could attract healthier clients with lower premiums. A serious health insurance sector began to emerge.

The connection between health insurance and employment was first forged in the midst of World War II, as a result of the Economic Stabilization Act of 1942.

With most young American men off to war, the government was concerned that employers would rapidly raise wages to attract the shrinking labor pool, thereby contributing to inflation and other economic problems. But while the 1942 law placed significant constraints on employers’ ability to raise wages, it did not restrict their ability to increase benefits. Employers took advantage of this loophole to introduce ever more generous health insurance as a fringe benefit — in lieu of the prohibited higher wages — to compete for the best workers.

In 1943, a federal court ruling asserted that direct payments by employers to insurers did not count as taxable employee income — meaning that any amount of an employee’s overall compensation dedicated to providing health insurance rather than direct cash wages would not be taxed.

This, of course, created an enormous financial incentive for employer-provided coverage.

The Internal Revenue Code reinforced this incentive in 1954 by explicitly exempting employer-sponsored health benefits from taxation. Employer-provided health coverage soon became a routine benefit.

Over the years, employer-sponsored insurance brought health care coverage to hundreds of millions of Americans. But the tax exemption for employer-sponsored plans also created massive problems that have endured to this day.

For one thing, employer-sponsored insurance makes many workers reluctant to leave unsatisfactory jobs for fear of losing their coverage. Those who fall ill while between jobs are burdened with the additional concern that a new insurance company might raise their premiums beyond what they can afford.

Insurers also face less competition and are less consumer-oriented, since they are at less risk of losing their customers. And, as noted above, because workers do not choose their own insurance, they are less likely to have plans that suit their needs.

The ACA ‘Cadillac tax’ on high-value health plans

Moreover, because employer-sponsored insurance is tax-exempt, employers have a major incentive to provide generous benefit packages. For example, a worker who pays federal and state income taxes at a combined rate of 30 percent will net $7,000 for every $10,000 his employer provides in gross salary. But the same employee will receive $10,000 in benefits for every $10,000 his employer spends on health insurance — a 43 percent improvement.

These generous benefits incentivize workers and employers to shift compensation away from cash wages, and into health care, even if those workers would benefit from higher wages. And by further divorcing workers from the cost and quality of the care they receive, the exclusion has encouraged hospitals and physicians to charge far higher prices in the United States than they do in other countries.

As noted above, The Joint Committee on Taxation — Congress’ in-house, non-partisan agency devoted to measuring the fiscal impact of tax-related legislation — has estimated that, in 2019, the federal government will subsidize employer-sponsored coverage by approximately $300 billion: the total amount of lost federal income taxes, Social Security payroll taxes, and Medicare payroll taxes that arise from the substitution of wage income with health benefits. In addition, state and local governments will lose an estimated $38 billion in 2019 tax revenue because of the employer tax exclusion.

At over $300 billion a year, then, the size of the tax expenditure for employer-sponsored coverage is the largest entitlement in the tax code, and the third-largest entitlement — next to Medicare and Medicaid — overall. Another notable feature of the employer tax exclusion is that it disproportionately benefits wealthy people. Those in the highest income-tax brackets benefit the most from the fact that their health benefits are excluded from taxation.

The Affordable Care Act attempts to gradually roll back the employer tax exclusion, by employing a “Cadillac tax” on high-value health plans.

Under the ACA, the tax was originally scheduled to go into effect in 2018; it applied a 40 percent excise tax on premiums that exceed $10,200 for single coverage and $27,500 for family coverage, with some adjustments and special-interest loopholes. These thresholds were set to increase in 2019 by a rate equivalent to the Consumer Price Index plus 1 percent (CPI+1%), and in 2020 and thereafter by the Consumer Price Index alone (CPI).

Congress has delayed the Cadillac tax several times. Under current law, it is set to become effective in 2022, applying a 40 percent excise tax on premiums that exceed $11,200 for single coverage and $30,150 for family coverage. Congress has also modified the tax so that businesses could count the tax as a deductible expense, thereby significantly reducing its bite.

Congress should streamline the Cadillac tax, by replacing it with a fiscally equivalent cap on the size of the employer tax exclusion, at thresholds comparable to those used in the Cadillac tax. Congress should eliminate most of the special-interest exceptions to the Cadillac tax that the ACA makes for particular labor unions, while preserving those in the new standard deduction for genuinely high-risk occupations such as law enforcement and fire protection.

Repealing the ACA’s employer mandate

The ACA also contains an employer mandate, requiring firms with 50 or more full-time workers to offer federally defined “minimum essential coverage” or pay a fine of $2,000 times the total number of full-time-equivalent employees at the firm, less 30.

The employer mandate represents unwise public policy, on a number of fronts.

First, it increases the cost for businesses to hire new workers, thereby acting as a drag on economic growth by increasing unemployment and the cost of goods and services.

Second, it perpetuates the inefficient linkage between health insurance and employment. As noted above, economists across the political spectrum have long advocated transitioning away from employer-sponsored insurance toward individually owned insurance.

Employer-sponsored coverage is costlier and less portable than individually owned coverage. Furthermore, employer-sponsored coverage is not tailored to the specific needs of individual employees but rather to the interests of the employer.

Third, the mandate has little to no impact on the number of people with health insurance, according to several non-partisan studies. An Urban Institute study published in July 2013 found “that the ACA can achieve all its major objectives without the employer mandate.” A follow-on study published in May 2014 estimated that the number of Americans with health insurance in 2016 would decline by a mere 0.08 percent if the mandate were repealed.

Fourth, transitioning from employer-sponsored coverage to individually purchased coverage would have a minor impact on the deficit. A March 2012 study by the Congressional Budget Office found that if an additional 14 million workers moved from employer-based to exchange-based coverage, the deficit would actually decrease by $13 billion over ten years. This is because the increase in exchange subsidies is offset by a reduction in lost revenue from the tax exclusion for employer-sponsored insurance.

In July 2013, the CBO estimated that a one-year delay of the employer mandate would increase spending on the exchanges by $3 billion, increase tax revenue by $1 billion due to an increase in taxable income, and reduce tax revenue by $10 billion due to the elimination of the employer mandate fine.

Fifth, the employer mandate gives firms a perverse incentive to avoid hiring low-income workers. According to the Medical Expenditure Panel Survey, 97 percent of firms with 50 or more workers already offer health benefits. 97 percent is not 100 percent, of course, and not all firms offer coverage to every employee. But the ACA’s employer mandate, perversely, incentivizes employers to avoid hiring low-income workers, precisely the type who tend to be uninsured.

As Robert Greenstein and Judith Solomon of the Center on Budget and Policy Priorities put it in 2009: “In essence, affected firms would pay a tax for hiring people from low- or moderate-income families.”

The penalties associated with the employer mandate are triggered only if a worker is not offered what the ACA deems “affordable” coverage, and if the worker then gains subsidized coverage on an ACA-sponsored insurance exchange.

The ACA thereby gives employers four incentives: (1) to hire fewer full-time workers; (2) to offer so-called unaffordable coverage, for which the penalties are lower; (3) to hire workers from high-income families, who are not eligible for subsidies; and (4) to hire illegal immigrants, who are also ineligible for subsidies.

In sum, the employer mandate penalizes firms for hiring low-income Americans. Through the Affordable Care Act, these individuals are able to gain subsidized health insurance. But they are tagged with a scarlet “S” — for gaining those subsidies — because, to employers, hiring subsidized individuals will be far more costly than hiring unsubsidized ones.

Transparency into the cost of employer-sponsored insurance

Workers have little visibility into the fact that their wages have stagnated due to the rising cost of health insurance. They falsely perceive that their coverage is “free,” and therefore are unable to make informed decisions about the relationship between the design of their health insurance plans and their cost.

While this problem has been mildly ameliorated by the fact that the IRS requires employers to disclose the value of employer-sponsored health coverage on workers’ W-2 forms, this is done in abstruse fashion, with workers needing to understand that Code DD in Box 12 represents the value of the health insurance that their employer sponsored on their behalf.

The Box 12 disclosure fails in two ways. First, it does not help the worker understand how his health insurance costs have risen over time, in comparison to his wages. A better disclosure would describe the progression of the worker’s wages over the entire tenure of his employment at a given firm, and also the progression of the cost of his health insurance.

In addition, because the disclosure comes on a W-2 form, and not in a more direct conversation with the worker’s employer, it fails to generate a constructive conversation between the worker and employer about how best to reduce the cost of health insurance in ways that the worker considers to be of most value.

In order to address these problems, Congress should require employers with more than 100 workers to send letters to their workers detailing their wages and health insurance costs for each calendar year they have been employed by the firm. This higher level of transparency can help workers to start to understand how the rising cost of health care affects them, and work with their employers to identify options for reducing costs.

Transparency into anticompetitive provider contracts

As we discuss extensively in Improving Hospital Competition: A Key to Affordable Health Care, one of the biggest drivers of the rising cost of private health insurance is the market power of regional hospital monopolies.

It is problematic enough that regional hospital monopolies have the power to demand high prices. But on top of this, many hospitals engage in additional anticompetitive practices. Anna Wilde Mathews of the Wall Street Journal obtained secret contracts between insurers and hospitals revealing that these contracts often barred insurers from sending patients to “less-expensive or higher-quality health care providers.” Other hospitals precluded insurers from excluding some of the system’s hospitals from the insurer’s networks. Some contract provisions, including those from New York-Presbyterian Hospital and BJC HealthCare of St. Louis, prevented insurers from disclosing a hospital’s prices to patients.

What’s clear is that the Federal Trade Commission simply does not have the bandwidth or the ability to enforce antitrust law when it comes to the thousands of insurer-hospital contracts in America. Subpoenaing each contract in order to review for anticompetitive language is infeasible, time consuming, and highly intrusive. A simpler solution would be to establish an all-payer claims database, with full transparency into payer-provider contracts within 60 days, so as to give the public the ability to identify anticompetitive practices. The claims database would serve the additional purpose of creating price transparency for private insurers, allowing more efficient competition, especially from new entrants and other startups.

Lowering the cost of employer-sponsored coverage

The Affordable Care Act’s impact on health insurance premiums is most greatly felt in the market for people who shop for coverage on their own: what economists call the individual or non-group market. This is because the employer-sponsored insurance market has already incorporated many of the premium-increasing features of the ACA.

For example, when employers purchase group coverage for their employees, insurers are typically required to offer coverage to everyone designated by the employer (guaranteed issue), with similar premiums regardless of health status (community rating).

However, some insurance regulations that affect the individual insurance market also affect the employer-sponsored market, especially the small group market.

Employer-sponsored insurance can be divided into three categories. The “small group” market applies to employers with an average of one to 100 total employees. The “large group” market encompasses employers with an average of more than 100 total employees.

There is a third category of companies: companies that take advantage of the Employee Retirement Income Security Act, or ERISA, to self-insure. Instead of paying premiums to an insurer, which then reimburses hospitals and doctors for incurred health claims, self-insured employers pay those claims directly. These self-insured ERISA plans are exempt from state insurance regulations, though they are subject to many of the ACA’s federal insurance regulations.

Small group plans, in particular, are affected by the ACA’s requirements regarding essential health benefits and medical loss ratios.

Hence, reforming many ACA provisions that affect the individual market also would reduce premiums in the employer-sponsored market.

In addition, to make employer-based coverage more affordable, Congress and the executive branch must take steps to reform the abuses of monopoly power in the hospital and pharmaceutical industries.

But ultimately, the most important ways to make employer-sponsored coverage more affordable is to evolve away from the group model and toward a system of consumer-driven, individually purchased health insurance.

{kind=link}